Reporting Going Concern Matters in the Auditor's Report

Frequently Asked Questions

IAASB

| Guidance & Support Tools

English

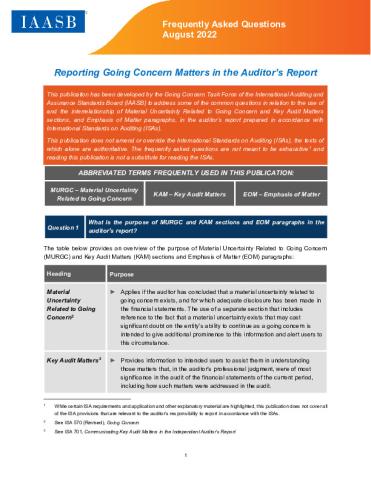

This non-authoritative Frequently Asked Questions publication addresses some of the common questions related to reporting going concern matters in the auditor’s report. Specifically, the publication focuses on the use of and interrelationship of the Material Uncertainty Related to Going Concern and Key Audit Matters sections, and the Emphasis of Matter paragraphs, in an auditor’s report prepared in accordance with the International Standards on Auditing (ISAs).

This publication does not amend or override the International Standards on Auditing, the texts of which alone are authoritative. Reading the publication is not a substitute for reading the ISAs.

Copyright © 2026 The International Federation of Accountants (IFAC). All rights reserved.